Tariffs and retaliation: a quantitative analysis

Par

Introduction

The introduction by the United States of extensive tariffs, established on the occasion of « Liberation Day, » on all of their trading partners should have considerable consequences on international trade, the American and global economies. These measures, although not yet fully implemented, consist of a universal base duty of 10%, as well as higher rates targeting countries with significant bilateral trade surpluses with the United States. If these tariffs are fully applied and maintained, they should deeply reshape existing trade relations and economic structures.

Table 1 presents the proposed tariff schedule for « Liberation Day » for several countries.

| Country | « Tariffs » on American Products | U.S. Tariff Response |

|---|---|---|

| China | 67% | 34% |

| European Union | 39% | 20% |

| Japan | 46% | 24% |

| South Africa | 60% | 30% |

| Vietnam | 90% | 46% |

For a large country like the United States, a tariff can increase welfare by improving the terms of trade, as the trade power of the United States in global markets can encourage its trading partners to accept lower prices in exchange for exports to the United States. But this tariff also represents a major macroeconomic shock, restricting the supply chains of intermediate imports and, to the extent that foreign exporters do not bear the full burden of adjustment, increasing consumer prices in the United States. However, it is very unlikely that the rest of the world will passively accept significant unilateral tariffs on its exports to the United States. It will certainly react with retaliatory tariffs. In this case, the benefits of the terms of trade for the United States would decrease, and the overall volume of world trade would diminish. Similarly, the macroeconomic effects of a global trade war would be highly restrictive. In recent articles (Auray, Devereux et Eyquem, 2024a, 2025a), we conduct an analysis of the effects of Liberation Day tariffs in a two-country neo-Keynesian model calibrated to represent the United States and the rest of the world (ROW). We simulate the short- and long-term effects of an unexpected permanent unilateral tariff imposed by the United States and an assumed equal response from the rest of the world. Our view is that the tariff shock and the retaliation will have two distinct impacts on the trade system and the global economy. The long-term impacts will be determined by the reduction in international trade, the shrinking of global supply chains, and the permanent distortion effects on domestic consumption and factor supply. In the shorter term, the tariff shock affects aggregate demand and inflation through its effect on production costs. The endogenous response of monetary policy to the shock is crucial for the magnitude of these effects.

Although the United States is the world’s largest economy, its share of global GDP is small, and, assessed bilaterally, it is more open to trade with the rest of the world than the rest of the world is with the United States. This implies that a tariff of equal size in both regions results in a more significant negative effect on output for the United States than for the rest of the world. Secondly, the response to a permanent tariff is much greater in the short term than in the long term. This is due to an endogenous monetary policy response to the surge in CPI inflation following the tariff shock. Finally, the presence of global supply chains in the form of imported intermediate goods is essential to the scale effect of the tariff response. The impact and long-term negative effects of the tariff shock would be considerably reduced in the absence of imported intermediate goods. Our article contributes to the recent assessment of the new tariffs announced and imposed by the new U.S. administration (see Attinasi et Mancini (2025), Baldwin et Barba Navaretti (2025) Conteduca et al. (2025), Evenett et Fritz (2025) Fajgelbaum et al. (2024) among others).

Modeling Approach

We describe a model with a home country and a foreign country, intended to represent the rest of the world and the United States, respectively. Firms use labor and traded intermediate goods to produce, and prices are rigid. The full description of the model is available in Auray, Devereux et Eyquem (2024b) and Auray, Devereux et Eyquem (2025b). Our approach is to quantify the effects of a significant, unexpected, and permanent increase in foreign tariffs on imported goods, on GDP, consumption, CPI inflation, and the terms of trade, the trade balance, and welfare in both countries. We add to this by assuming a one-for-one retaliation from the home country. The share in the world population and in world GDP do not coincide because countries potentially differ in terms of GDP per capita. We therefore reproduce both the population share of the USA and the share of the USA’s GDP in the world population and world GDP, respectively, by adjusting GDP per capita. We calibrate so that the relative size of the foreign country corresponds to the American population (0.083). We assume a trade openness in the United States of 25% with an initial base tariff rate of 5%. 0.4 is the elasticity of production to the quantity of intermediate goods. With a Cobb-Douglas function, this corresponds exactly to the share of spending on intermediate goods in production. The share of intermediate goods in production is therefore 40%, according to Bergin and Corsetti (2023). The elasticity of substitution between a domestic good and a foreign good is 5, according to Feenstra et al. (2018). Monetary policy takes the form of a Taylor rule with a coefficient of 1.5 on CPI inflation.

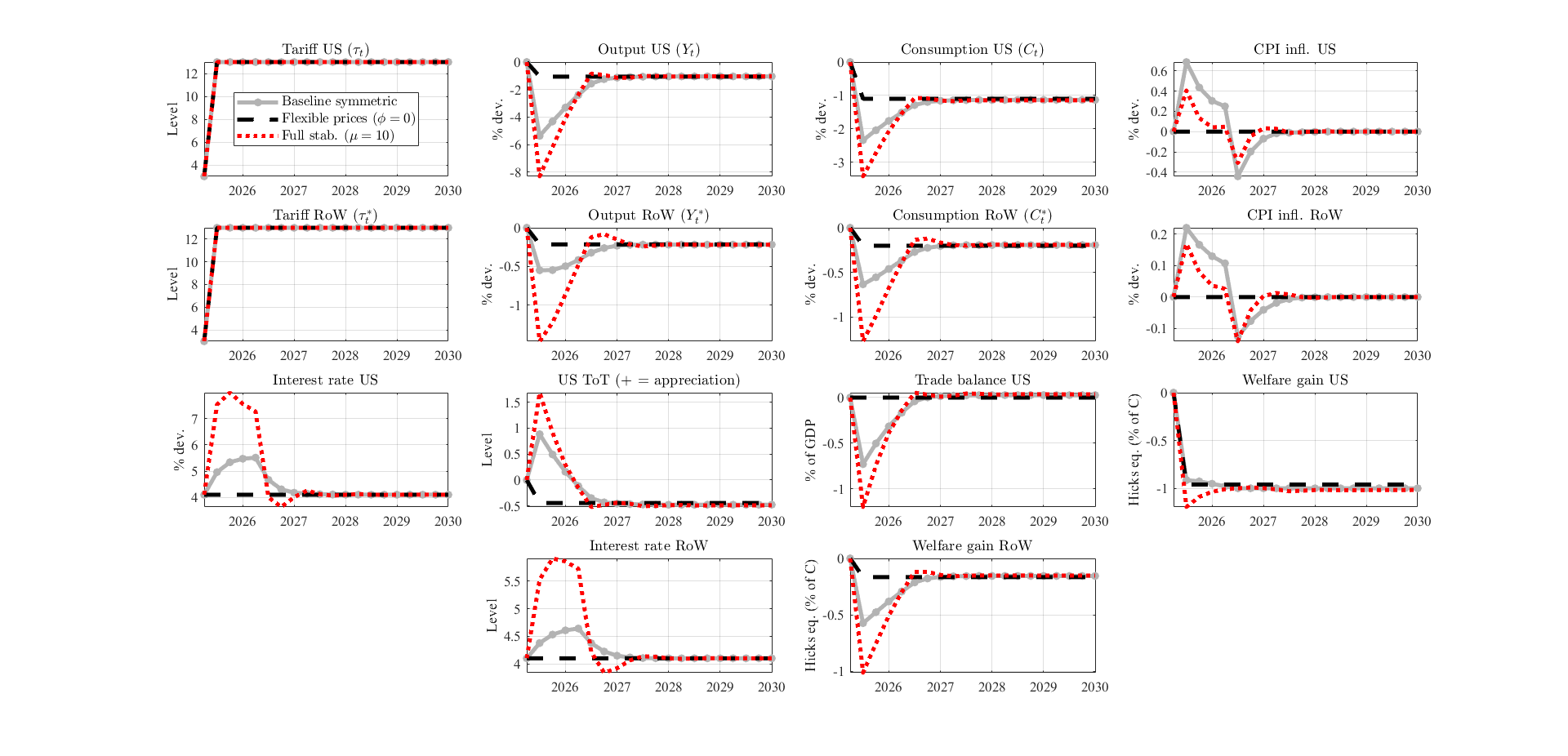

The graphique 1 presents our benchmark results (black curve and without retaliatory measures). A 10% increase in U.S. tariffs without retaliation reduces U.S. output by nearly 3% at impact, reducing U.S. consumption by 0.5%. It increases U.S. CPI inflation by 0.3%, leading to an increase in the U.S. policy rate of more than 60 basis points. The U.S. terms of trade appreciate, but the price of intermediate imports increases. This is a key factor in the decline of U.S. output. This sharp decline in output, with a moderate effect on consumption, leads to a significant deterioration in the U.S. trade balance at impact. Although U.S. output and consumption decrease, in terms of welfare, U.S. households experience a gain of about 0.5% in consumption-equivalent terms at impact (0.4% in the long term), mainly due to the reduction in their labor supply. In contrast, households in the rest of the world experience an equivalent welfare loss at impact—about 0.5% of consumption equivalent—although this loss gradually converges to its long-term value of 0.26% after a few quarters. The graphique 1 also shows that after the increase in U.S. tariffs, the output of the rest of the world decreases only slightly. Their exposure to trade with the United States is much lower than that of U.S. households, as indicated in the model calibration section. While these results are instructive, the unilateral scenario is not the most plausible. Assuming that the rest of the world adopts equivalent retaliatory tariffs, the negative effects on U.S. output, consumption, and inflation are much greater. Although U.S. tariffs are fully offset by those of the rest of the world, the terms of trade still move in favor of the United States, due to the asymmetry in openness between the United States and all other countries. But U.S. consumers now suffer a greater welfare loss than that suffered by the rest of the world. Why does the symmetric increase in tariffs affect the U.S. economy much more harshly than that of the rest of the world? Because the United States relies much more on trade with the rest of the world than vice versa, it is disproportionately affected. This underscores the importance of a coordinated response from the rest of the world to U.S. tariffs. Although the United States is the world’s largest economy and the primary export market for many countries, it accounts for only a small share of the global economy and trade. This point is illustrated by an alternative calibration in the graphique 1 (red dotted case), which is based on the counterfactual assumption of a tariff with full retaliation, if not to assume two countries of equal size. In this case, the decline in U.S. output is much less than in our benchmark scenario with retaliation, and of course, the trade balance and the terms of trade are not affected.

Alternative Assumptions on Supply Chains and Pricing

To illustrate the importance of the different mechanisms in our model, we examine two alternative calibrations. The graphique 2 illustrates the response to the trade war in the absence of intermediate goods in production, assuming that production is solely ensured by labor (no capital). If the qualitative response of output, terms of trade, and the trade balance is similar to that of the benchmark scenario, the scale is noticeably different. The output of both countries decreases much less than in the benchmark scenario. This highlights the importance of intermediate imports in production and the role of supply chains in amplifying the effect of the tariff shock.

The second variant we examine concerns the importance of the monetary policy response. To highlight this mechanism, the graphique 3 assumes totally flexible prices, so that monetary policy plays no role in the adjustment process. In both countries, output and consumption decrease much more gradually before converging to their negative long-term value. The U.S. terms of trade actually deteriorate, due to the decrease in U.S. consumption, with a national bias in consumption habits, and the trade balance remains virtually unchanged. Although the long-term dynamics are identical to those of the benchmark model, the negative effects of tariff shocks are much greater when firms cannot instantly adjust their prices. This demonstrates one of the major contributions of our analysis: it highlights the importance of price rigidity and the monetary policy response to the tariff shock in shaping short-term responses to the tariff shock and global retaliation. Finally, this figure shows similar but quantitatively more significant results in the case of a full monetary policy adjustment.

Table 1 summarizes our results and presents the short- and long-term effects of the unilateral and full retaliation scenarios. Overall, the short-term results reveal significant negative effects on U.S. output, ranging from -0.5% to over -7%. In the most likely case (2nd column), output falls by 2.4%. The inflationary effects range from zero (flexible prices or full stabilization monetary policy) to over 0.6 percentage points. The increase in tariffs generates welfare gains for U.S. consumers only in the unilateral case; all other cases result in moderate to significant welfare losses—the largest loss, 3.8%, occurring when U.S. imports are less substitutable than foreign imports. Similarly, in almost all cases, the increase in tariffs generates trade deficits in the United States. As we have already discussed at length, the effects in the rest of the world are much more moderate, though not negligible. The table (part b) also presents the results after 5 years. After 5 years, the economies have almost converged to their new long-term values induced by the tariffs. From a qualitative perspective, the evolution of output and consumption is very similar but slightly weaker, with the short-term dynamics and amplification induced by monetary policy having disappeared. U.S. output continues to decrease substantially—between -0.8% and -3.3% depending on the case. U.S. consumption is also well below its pre-tariff increase level—except in the case of unilateral tariff setting—and U.S. consumers experience moderate to significant welfare losses.